Find construction insurance quotes

Save money by comparing quotes from trusted insurance providers.

Construction companies can save money on business insurance by comparing quotes from different providers with Insureon. Your premium depends on the type of policy, coverage limits, deductibles, and factors such as your business's location and number of employees.

Here are the top policies purchased by construction businesses and their average monthly costs:

Our figures are sourced from the median cost of policies purchased by Insureon customers. The median offers a better estimate of what your business is likely to pay because it excludes outlier high and low premiums.

Construction businesses pay an average of $89 per month, or $1,069 annually, for general liability insurance.

General liability insurance provides financial protection against common lawsuits from customers. It can cover costs if someone sues your business for a bodily injury, property damage, or copyright infringement.

This is the average policy for construction professionals who buy from Insureon:

Insurance premium: $89 per month

Policy limits: $1 million per occurrence; $2 million aggregate

Deductible: $500

Small businesses can often save money by bundling general liability coverage with commercial property insurance in a business owner’s policy (BOP).

The cost of general liability insurance depends on factors such as the coverage limits you choose, the size of your business, the amount of foot traffic you have, and any subcontractors or additional insured endorsements.

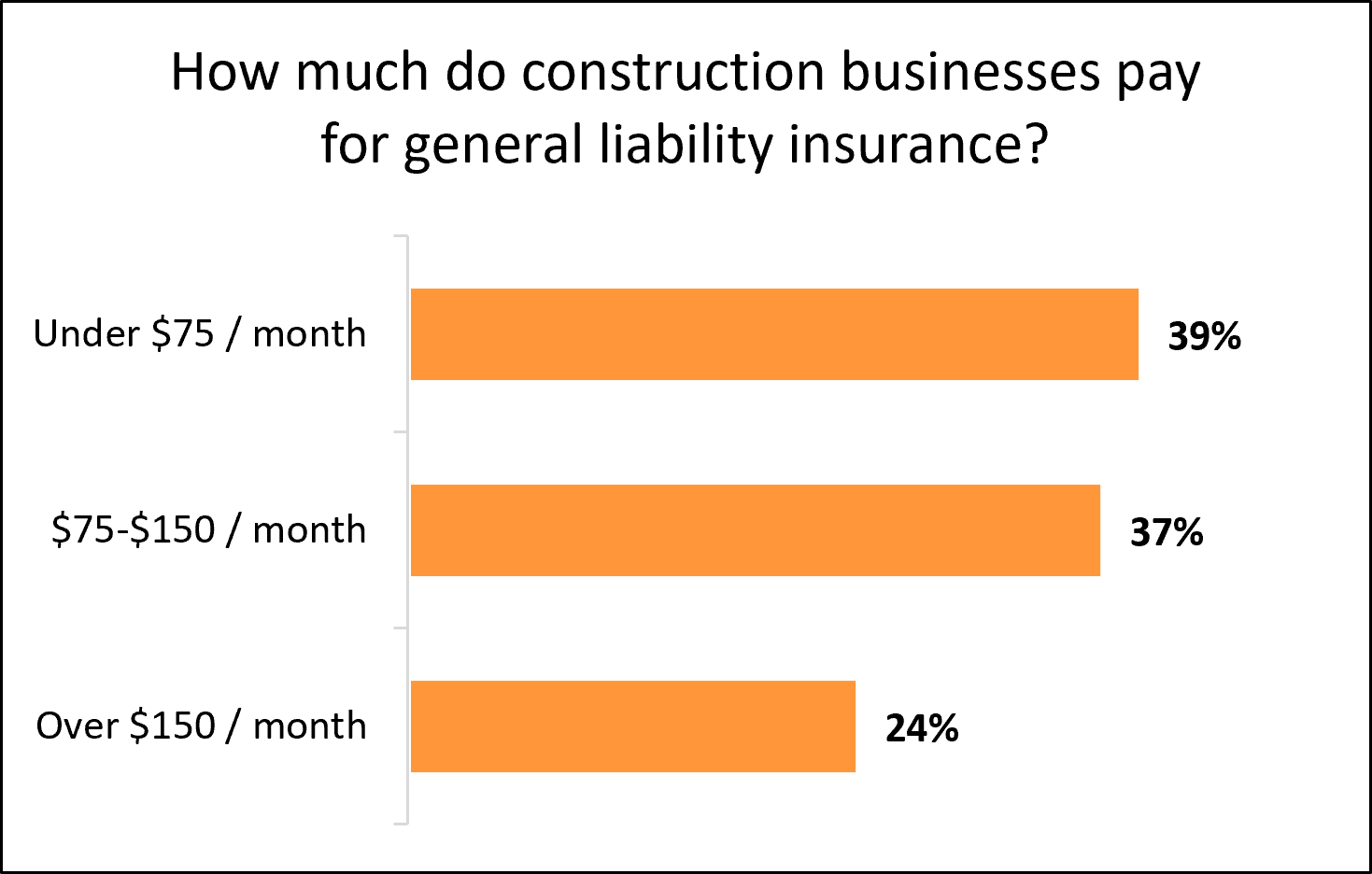

The cost of general liability insurance depends on your risk of a customer lawsuit. Among construction businesses and contractors that purchase general liability insurance with Insureon, 39% pay less than $75 per month, and 76% pay less than $150 per month.

Businesses that interact with many customers and have a higher risk of accidents typically pay more for general liability insurance.

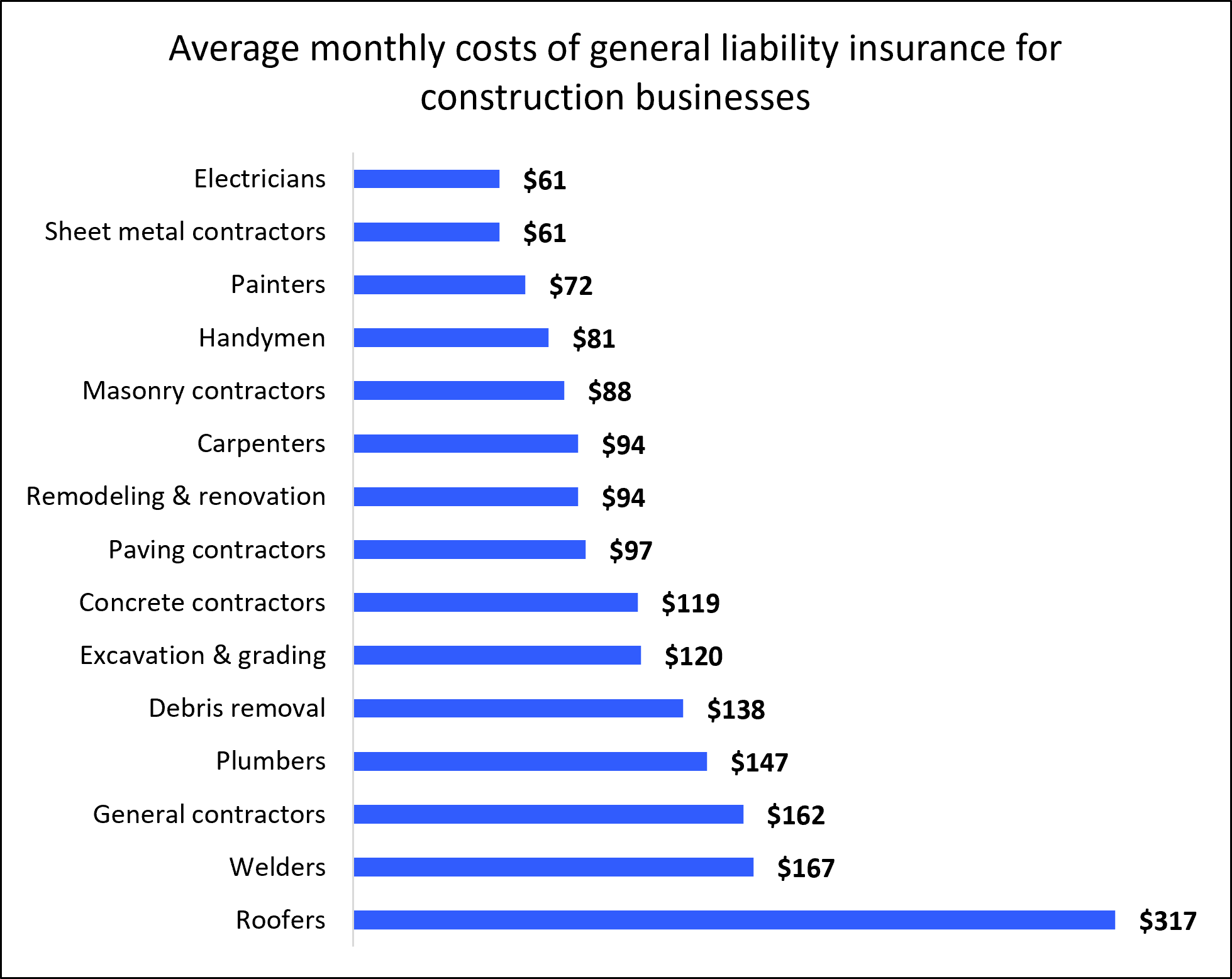

For example, roofers can expect to pay more for general liability insurance than a profession with more moderate risk, such as general contractors. Similarly, a general contractor will often pay a higher premium for this coverage than electricians and other lower-risk professionals.

The average cost of general liability insurance for a roofer is $317 per month, while general contractor insurance rates fall closer to an average of $162 per month, and electricians will pay just $61 per month on average for coverage.

Other factors that affect your premium include business revenue, building maintenance, years in operation, and location. As you can see, the cost varies significantly across professions.

Policy limits are the maximum amounts your insurance company will pay for covered claims.

The per-occurrence limit is the maximum your insurer will pay for a single incident, while the aggregate limit is the maximum your insurer will pay on any claims during your policy period, typically one year. Higher limits cost more – and provide better coverage.

Most contractors and construction businesses (92%) choose general liability insurance policies with a $1 million per-occurrence limit and a $2 million aggregate limit. As your small business grows, you may need to expand your policy limits.

Learn more on how to save money on your policy.

Construction businesses pay an average of $125 per month for a business owner's policy, or $1,503 annually. Most choose a BOP with a $1 million per-occurrence limit and a $2 million aggregate limit.

A BOP bundles general liability coverage with commercial property insurance at a discount. It provides financial protection against common lawsuits from customers and also covers the cost of stolen, damaged, or destroyed business property.

The cost of a business owner's policy depends on factors such as the limits you choose, the size of your business, the amount of foot traffic you have, and the value of your business property and equipment.

Construction businesses pay an average of $175 per month, or $2,101 annually, for workers’ compensation insurance.

Workers' comp is a key policy in construction, as workers face a high risk of injury. It helps cover medical expenses from job injuries, which your personal health insurance might exclude. It also supplies partial lost wages during recovery in the form of disability benefits.

Most policies include employer's liability insurance, which covers the cost of lawsuits related to workplace injuries.

There's usually no limit to how much a workers' comp policy can pay for employee benefits, though it depends on state laws.

The cost of workers' compensation insurance depends on several factors, including the number of employees you have and the level of risk involved with their jobs.

Get more information on how to save money on your workers' comp policy.

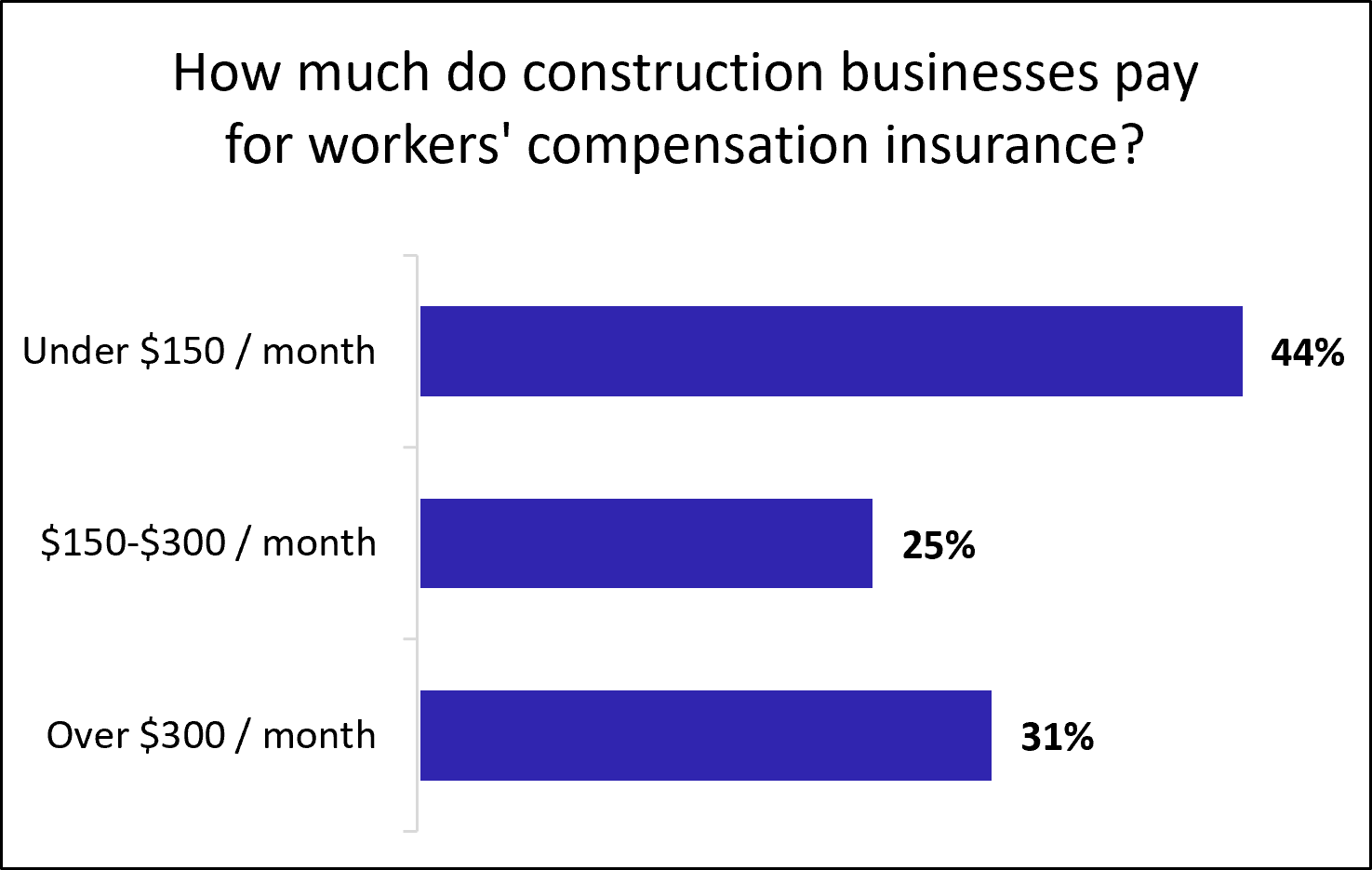

Among construction businesses and contractors that purchase workers’ compensation insurance with Insureon, 44% pay less than $150 per month and 69% pay less than $300 per month.

A larger workforce brings a higher risk of worker injuries, which is why bigger businesses tend to pay more for this type of insurance.

Construction businesses pay an average of $268 per month for commercial auto insurance, or $3,212 annually.

Most states require this coverage for vehicles owned by a business. For personal, rented, and leased vehicles used by your business, look to hired and non-owned auto insurance (HNOA) instead.

A commercial auto policy provides financial protection in the event of an accident involving your business vehicle. It can help pay for property damage, medical costs, and legal expenses.

The cost of commercial auto insurance depends on several factors, including the policy limits you choose, coverage options, the value of the vehicle, and the driving records of anyone permitted to drive.

Construction businesses pay an average of $67 per month for professional liability insurance, or $808 annually. This policy is occasionally required by state law, though it's more often needed for licenses and contracts.

Professional liability insurance covers the cost of lawsuits from clients who sue over a mistake, missed deadline, or breach of contract. It's sometimes referred to as errors and omissions insurance (E&O).

Construction contractors who buy this coverage from Insureon can often bundle it with general liability insurance for a discount. The average cost of this bundle is $150 per month for Insureon customers.

The cost of professional liability insurance depends on several factors, including the type of business you have, your claims history, and the policy limits you choose.

Get more information on how to save money on your professional liability insurance.

On average, construction businesses pay $42 per month, or $505 annually, for tools and equipment insurance.

Also called inland marine insurance, this policy covers the cost of lost, stolen, or damaged tools and equipment. Unlike standard property insurance, it protects your items while they're in transit, at a customer's home, or stored off-site.

The cost of tools and equipment coverage depends on the value of your tools and equipment and the type of work you do.

Construction businesses pay an average of $93 per month for commercial umbrella insurance, or about $1,111 annually.

This policy boosts the limits of your underlying general liability, commercial auto, or employer's liability insurance. When the underlying policy reaches its limit, commercial umbrella insurance activates to cover any costs over that limit.

The cost of commercial umbrella insurance depends primarily on the amount of coverage you purchase.

Construction businesses pay an average of $136 per month for builder's risk insurance, or about $1,635 annually. This policy is sometimes called course of construction insurance.

A builder's risk insurance policy provides coverage for structures and materials during a construction project. It will help pay for fires, vandalism, and other types of damage to a structure in progress.

The cost of builder's risk insurance depends on the value of the structure, including materials and labor.

Construction businesses pay an average of $9 per month for surety bonds, or about $112 annually. A surety bond reimburses your client if you're unable to fulfill the terms of a contract or other agreement.

The cost of a surety bond is a percentage of the total bond amount. It may also be influenced by your type of work and your credit score.

Your insurance provider calculates your construction business insurance premiums based on several factors, including:

Insureon works with top-rated U.S. providers to find affordable insurance coverage that fits your business. Apply today to get free quotes with one easy online application. A licensed insurance agent who specializes in your profession's unique risks will help you find the right coverage and answer any questions.

Typically, you can get a certificate of insurance (COI) within 24 hours of submitting your application.

The average costs on this page were derived from our data of 40,000+ small business owners in the construction field who purchased policies through Insureon. Most of our customers have less than five employees, annual revenue ranging from around $50,000 to more than $200,000, and five years or less in business.

By entering your email address and subscribing, you agree to our Terms of Use and Privacy Policy