Get insurance quotes for agents and brokers

Save money by comparing insurance quotes from multiple carriers.

The cost of business insurance for insurance agents depends on several factors, including the size of your business and its risks. Cost estimates are sourced from policies purchased by Insureon customers.

Here are the top commercial insurance policies purchased by insurance agents and other insurance professionals and their average monthly costs:

Our figures are sourced from the median cost of small business insurance policies purchased by Insureon customers who are insurance specialists, such as agents and brokers, claims adjusters, and actuaries. The median offers a better estimate of what your business is likely to pay because it excludes outlier high and low premiums.

The cost of business insurance depends on a number of factors. This includes the types of insurance services and products you offer, your annual revenue, the value of your business property and equipment, your location, your business size, and the policy limits and deductibles you select.

Insurance agents, brokers, and other insurance professionals pay an average of $65 per month, or $781 annually, for errors and omissions (E&O) insurance. This policy is sometimes referred to as professional liability insurance.

An errors and omissions insurance policy offers critical coverage for insurance businesses, including paying for legal fees related to accusations of professional negligence.

For example, if an insurance agent fails to secure flood coverage for a homeowner who lives in an area prone to flooding, this policy would cover their attorney fees and other legal costs in the event of a lawsuit. It would also cover your business if you make errors or oversights that result in financial loss for your client.

This is the average E&O policy for insurance agents and other insurance businesses that buy from Insureon:

Premium: $65 per month

Policy limits: $1 million per occurrence; $1 million aggregate

Deductible: $1,000

The cost of errors and omissions insurance for insurance professionals depends on several factors.

This includes the types of insurance products and services you offer, your business size and revenue, the coverage limits and deductible you choose, your claims history, where you're located, and your insurance specialty (such as, property and casualty insurance, life insurance, health insurance, etc.).

Among insurance businesses that purchase an E&O insurance policy with Insureon, 41% pay less than $50 per month and 72% pay less than $100 per month.

Insurance professionals, including agents and brokers, who work with higher-risk clients or specialize in certain areas may pay higher premiums due to their unique risks. Insurance companies will look at the type of professional services you offer and your insurance firm's overall risk level when underwriting your premium.

Across all insurance professions, learn how to get cheap errors and omissions insurance.

Policy limits are the maximum amounts your insurance company will pay for covered claims.

The per-occurrence limit is the most your insurer will pay for a single incident, while the aggregate limit is the maximum your insurer will pay on any claims during your policy period, typically one year.

Most insurance businesses (83%) choose errors and omissions policies with a $1 million per-occurrence limit and a $1 million aggregate limit.

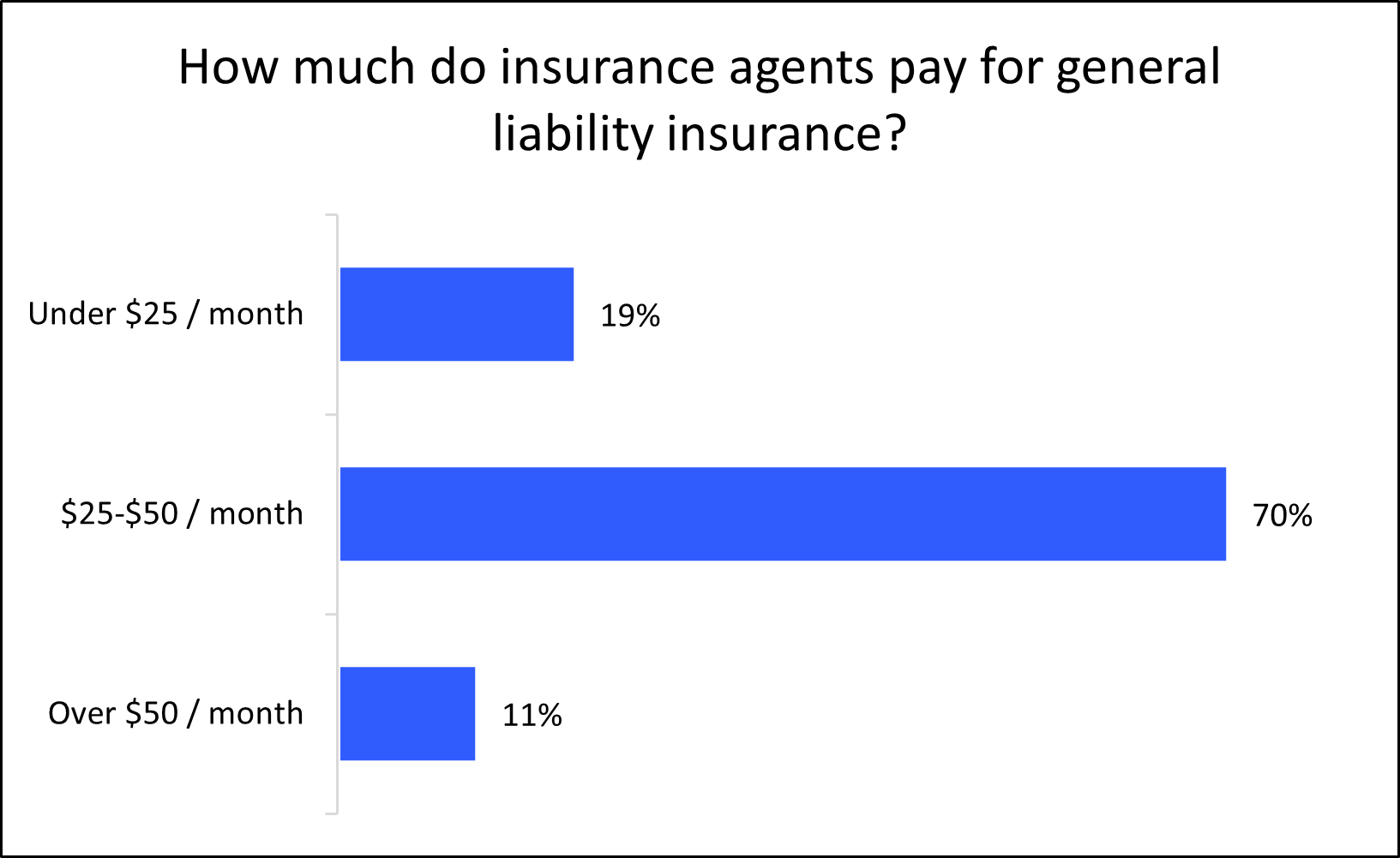

Insurance agencies pay an average of $29 per month, or $350 per year, for general liability insurance.

General liability insurance helps cover legal fees related to common third-party lawsuits from clients, including those related to bodily injuries, property damage, and advertising injuries. For example, a client could slip on a wet floor in your office and then sue your business to recoup the cost of medical treatment for their injury.

This is the average general liability policy for insurance agents and other insurance specialists who buy from Insureon:

Insurance premium: $29 per month

Policy limits: $1 million per occurrence; $2 million aggregate

Deductible: $500

The cost of general liability insurance depends on several factors, such as the coverage limits you choose, the size of your business, the amount of foot traffic you have, your location, and any endorsements on your policy, such as an additional insured.

General liability insurance costs increase with the likelihood of customer lawsuits, such as someone suing your business over a slip-and-fall injury. That's why businesses with an office that is open to the public can expect to pay more for this coverage than a home-based business.

This leads to a wide range of insurance premiums for different professions. Among insurance companies that purchase general liability insurance with Insureon, 89% pay less than $50 per month.

Most insurance businesses (89%) choose general liability policies with a $1 million per-occurrence limit and a $2 million aggregate limit. As your small business grows, you may need to expand your policy limits.

Insurance agencies and other insurance firms pay an average of $45 per month, or $542 per year, for a business owner’s policy.

A business owner's policy, or BOP, bundles general liability coverage with commercial property insurance to cover both third-party risks and your business property. It typically costs less than purchasing each policy separately.

A BOP protects against client injuries and property damage. In addition, this type of insurance covers the repair or replacement costs of your physical building and office equipment if they're damaged due to vandalism and other covered claims.

Because of its increased coverage and affordability, it’s the policy most often recommended by Insureon’s agents for small business owners who rent or own a building.

This is the average BOP for insurance businesses that buy from Insureon:

Insurance premium: $45 per month

Policy limits: $1 million per occurrence; $2 million aggregate

Deductible: $500

Small, low-risk insurance companies are often eligible for a business owner's policy.

Small business owners may see higher costs if they choose to add endorsements to their policy. Insurance endorsements, such as business interruption insurance or equipment breakdown coverage, are often recommended to help avoid financial losses if a fire or power outage forces your business operations to cease for an extended period of time.

The cost of a business owner's policy is based on a number of factors. That includes the value of your property, where you are located, the number of employees you have, and your specialty.

Insurance agencies with larger or more expensive business property will typically pay more for a BOP than those with smaller premises or lower value business property.

Your industry risk, years in operation, and claims history will also affect your insurance rates.

For insurance businesses, workers’ compensation insurance costs an average of $39 per month, or $469 per year.

This insurance policy covers medical expenses when an employee is injured on the job, and it also provides disability benefits while they're recovering and unable to work.

To comply with your state’s requirements and avoid penalties, businesses with employees typically must purchase this coverage. It's also recommended for sole proprietors, as health insurance plans can deny claims for medical bills when an injury or illness is related to your job.

Most policies include employer's liability insurance, which covers the cost of lawsuits related to workplace injuries. There's usually no limit to how much a workers' comp policy can pay for employee benefits, though it depends on state laws.

The cost of workers' compensation insurance depends on several factors, including the number of employees you have and the level of risk involved with their jobs.

Get more information on how to find affordable workers' compensation coverage.

Among insurance companies that buy workers’ compensation insurance with Insureon, 31% pay less than $30 per month and 81% pay $60 or less per month.

Workers' comp costs depend on the number of employees you have in your small business. A larger workforce brings a higher risk of work-related injuries, which is why bigger businesses tend to pay more for this type of insurance.

Insurance agents and other types of insurance business owners pay an average of $71 per month, or $850 annually, for cyber insurance. This policy is also called cyber liability insurance or cybersecurity insurance.

Cyber insurance helps businesses recover financially after a data breach or cyberattack. It can help pay for customer notification costs, fraud monitoring services, and other expenses necessitated by state data breach laws.

The cost of cyber insurance depends on the amount of sensitive information handled by your insurance agency, such as client Social Security numbers and credit card information, along with the number of employees who can access that information.

Small businesses, including insurance agencies and other types of insurance companies, pay an average of $245 per month, or $2,942 annually, for commercial auto insurance.

Most states require this liability insurance coverage for vehicles owned by an insurance agency. For personal, rented, and leased vehicles used by your business, look to hired and non-owned auto insurance (HNOA) instead.

A commercial auto policy provides financial protection in the event of an accident involving your business vehicle. It can help pay for property damage, medical costs, and legal expenses.

The cost of commercial auto insurance depends on several factors, including the policy limits you choose, coverage options, the value of the vehicles, the driving records of anyone permitted to drive, and additional insured endorsements you select.

Learn more about how to find affordable commercial auto insurance coverage.

Insureon works with top-rated U.S. providers to find affordable insurance coverage for insurance businesses, whether you work independently or own an agency with employees.

Apply today to get free quotes with our easy online application. A licensed insurance agent who specializes in your profession's unique risks will help you find the right types of coverage for your business needs. Typically, you can get a certificate of insurance within 24 hours of submitting your application, offering instant peace of mind.

By entering your email address and subscribing, you agree to our Terms of Use and Privacy Policy